.png)

Your ability to earn a paycheck is one of the biggest assets you'll ever have — and an illness or injury can interrupt it without warning. Most working Americans couldn't go long without their income. If you work and collect a paycheck, you most likely need disability coverage to keep the bills paid while you recover.

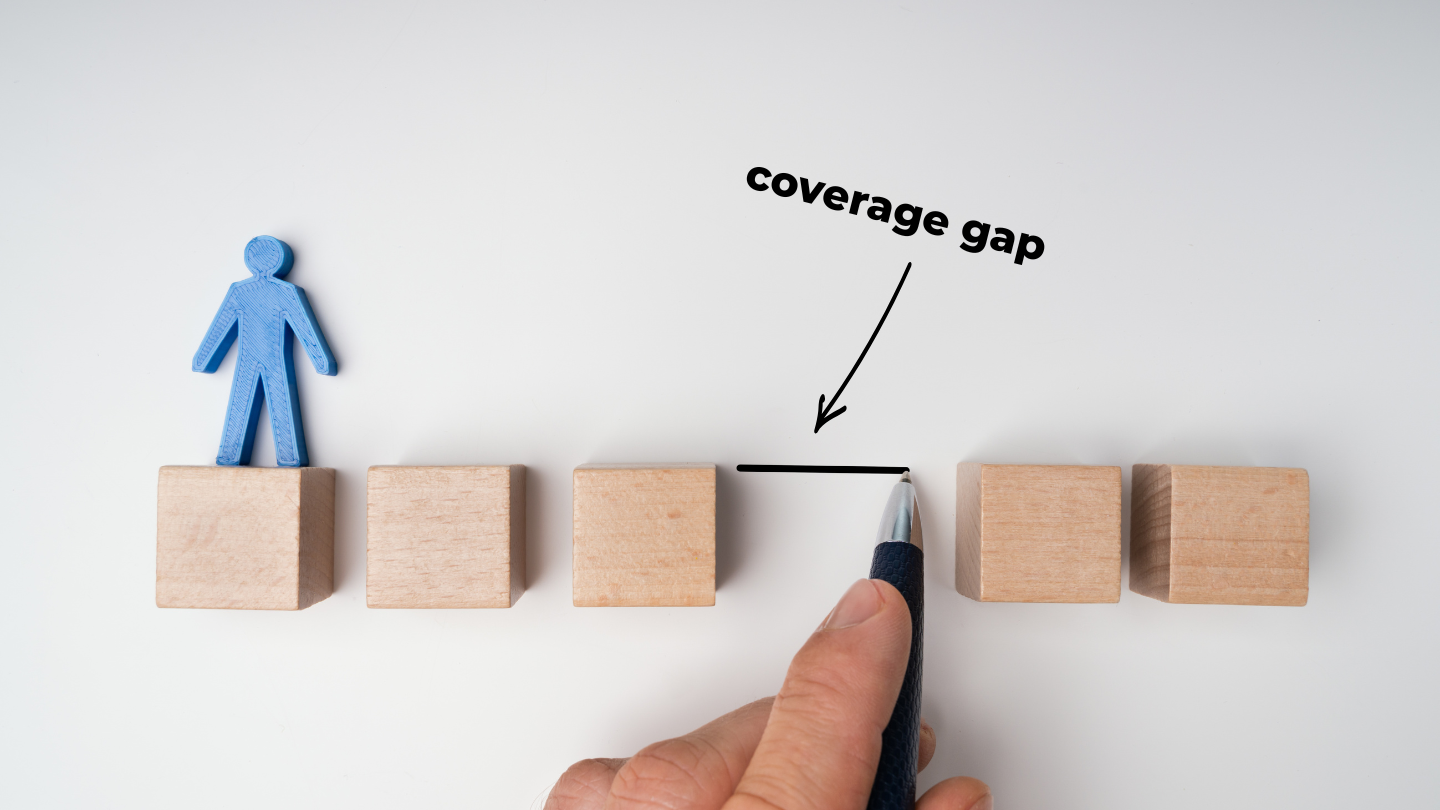

Most people assume something would catch them if they couldn't work — but the pieces rarely add up to a full paycheck. Workers' comp only applies to job-related injuries, state and Social Security benefits can be limited and slow, and employer coverage often replaces just a portion of your income. Individual disability insurance is what fills the gap and keeps your household running.

It's also worth revisiting after big life events — a new job, a mortgage, a growing family, or a jump in income — since your coverage should keep pace with what you'd need to replace.

A disabling illness or injury can feel remote — until you look at the odds.

A working person's chance of a disability that keeps them off the job 90 days or longer.

Most disabilities are caused by illnesses — not accidents.

One in four of today's 20-year-olds will become disabled before they retire.

Seven of ten working Americans couldn't get by for long without their next paycheck.

A 25-year-old earning $50,000 a year could lose $3.8 million in future earnings to a permanent disability.

Recovery can take months or years — coverage should reflect more than a short gap.

Coverage is subject to underwriting and is not bound or altered until confirmed by an authorized representative. Statistics are industry figures shared for education only. This page is a general overview, not a contract or a quote — contact a local Top O' Michigan agent for the coverage that fits your situation.

Disability income insurance replaces part of your paycheck if an illness or injury keeps you from working. Research commonly cited by the Social Security Administration suggests about 1 in 4 of today’s 20-year-olds will experience a disability before retirement — so it protects the income everything else depends on.

Only partly. Workers’ compensation covers job-related injuries only, state and Social Security disability can be limited and hard to qualify for, and employer coverage may not be enough on its own. An individual policy helps fill those gaps.

Policies commonly replace around 60% of your income, though the exact amount, waiting period, and benefit length depend on the plan you choose. A local agent helps you match it to your budget and needs.

Short-term typically covers a few weeks to several months after a waiting period; long-term can continue for years or until retirement. Many people layer both, and we can help you decide what fits.

It’s a great base, but employer coverage is often limited and isn’t always portable if you change jobs. An individual policy adds lasting protection that moves with you.

Let's make sure your income is covered if life throws a curveball. Talk with a local Michigan agent today.