.png)

People are more litigious than ever, and one simple accident can reach past your home and auto limits — threatening your savings, your income, even your ability to retire. A personal umbrella is an affordable way to add a layer of liability protection over everything you’ve worked for.

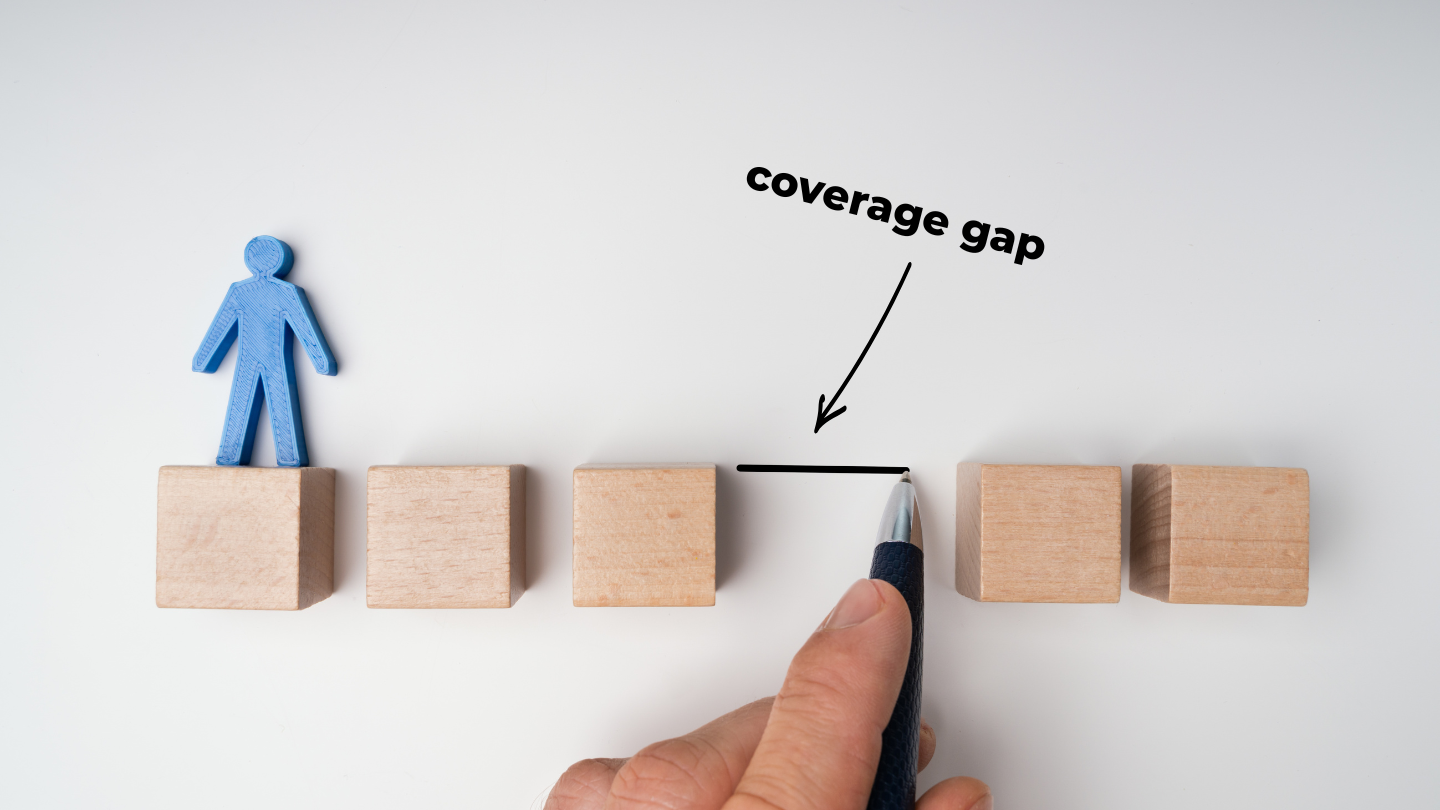

Your home and auto policies each include liability coverage — but only up to their limits. If a serious claim or lawsuit runs past those limits, the rest can come out of your own pocket. An umbrella policy “drops down” to add protection above your existing coverage, and it provides legal defense coverage when you need it most.

An attorney may charge $250 an hour. For roughly that same amount over a whole year, an umbrella can help protect your income and assets from a claim you never saw coming.

Video: Why Personal Umbrella Insurance Matters.

This short video walks through how a personal umbrella policy adds an extra layer of liability protection on top of your existing auto and homeowners coverage.Here's what it covers:- The coverage gap (0:22): If you're sued for damages that go beyond the liability limits on your primary auto or homeowners policy, you could be personally responsible for the difference.

- How an umbrella policy works (0:33): It acts as a safety net, helping cover costs once your underlying policy limits have been used up — subject to the terms of your policy.

- A real-world example (0:41): Say you're found at fault in an auto accident with $1,000,000 in damages but carry $500,000 in auto liability coverage. An umbrella policy may help cover the remaining $500,000, depending on your policy.

- More than just accidents (1:20): Umbrella coverage can also apply to situations like a slip-and-fall on your property, a dog bite, or claims of libel, slander, and defamation of character.

- Help with legal costs (1:43): An umbrella policy may also assist with defense and legal fees, which can add up quickly during a lawsuit.The takeaway: you don't have to be a millionaire to be sued like one. Coverage and eligibility are subject to underwriting, so the best next step is to talk with one of our independent agents about the protection that fits your situation. Call us at 800-686-8664 to get started.

If you have assets or income to protect, an umbrella is worth a conversation. It’s especially worth a look if you…

With a steady income or retirement savings worth protecting.

Own or use vehicles, boats, or recreational equipment.

Including new and student drivers in the household.

Own animals, firearms, a pool, or a trampoline.

Added liability that reaches beyond a basic policy.

Use social media, volunteer, coach, or carpool.

Umbrella coverage is often one of the most cost-effective policies you can add — a relatively small premium for a meaningful layer of protection. A local Top O’ Michigan agent can look at your home, auto, and the rest of your picture and show you what makes sense for your family.

Coverage descriptions on this page are general and subject to underwriting and the terms of the policy you purchase. Insurance is not bound or altered until you receive confirmation from an authorized representative. Contact a local Top O’ Michigan agent for a quote.

A personal umbrella adds a layer of liability protection above your home and auto limits. If a serious claim goes beyond those limits, the umbrella picks up where they leave off (commonly $1M or more) and can add legal defense costs. Coverage is subject to underwriting.

If you own a home, drive or boat, have savings to protect, keep a pool or pets, host guests, or own rental property, it’s worth considering. It’s one of the more affordable ways to protect your assets from a large liability claim.

A common starting point is $1 million, with higher limits available. Many people choose a limit that roughly covers their net worth and risk exposure. A local agent can help you right-size it.

It’s liability coverage, so it doesn’t pay for your own property damage or injuries — it steps in for liability claims above your underlying policies. Carriers usually require minimum home and auto limits beneath it.

It’s typically one of the lower-cost coverages for the protection it provides, since it sits above your existing policies. Exact pricing is subject to underwriting — ask your agent for options.

It only takes a short conversation to see whether an umbrella makes sense for you — and what it would add over your home and auto coverage.